How a regular 9-to-5 employee earns passive income for financial independence

Dividend Investing in Singapore vs USA: What I’ve Learned

Over the last decade I’ve owned both Singapore and US dividend names. On the Singapore side: OCBC (O39.SI) and CapitaLand Integrated Commercial Trust / CICT (C38U.SI). In the US: Wells Fargo (WFC) and Realty Income (O).

Here’s what the total return picture (price change plus dividends reinvested) looks like over ~10 years and the key lessons that changed how I invest.

First, a crucial tax difference

- Singapore: For individuals, dividends from Singapore-resident companies are tax-exempt, and capital gains are generally not taxed. That means what you receive from OCBC or CICT lands in your pocket without personal income tax, and gains from selling your shares aren’t taxed (unless you’re considered to be trading).

- USA (for Singapore investors): Dividends from US stocks are typically hit with a 30% withholding tax (because there is no US–Singapore treaty), even after you file a W-8BEN with your broker. Capital gains on US shares are not taxed by the US for non-residents.

Bottom line: Singapore names enjoy a powerful net-income advantage on dividends; US names pay a “dividend tax drag” of 30%.

How the four picks actually did (past ~10 years)

Total return = price performance + dividends reinvested. This is the fairest way to judge dividend stocks across markets.

1) Bank vs Bank:

OCBC (O39.SI)

vs

Wells Fargo (WFC)

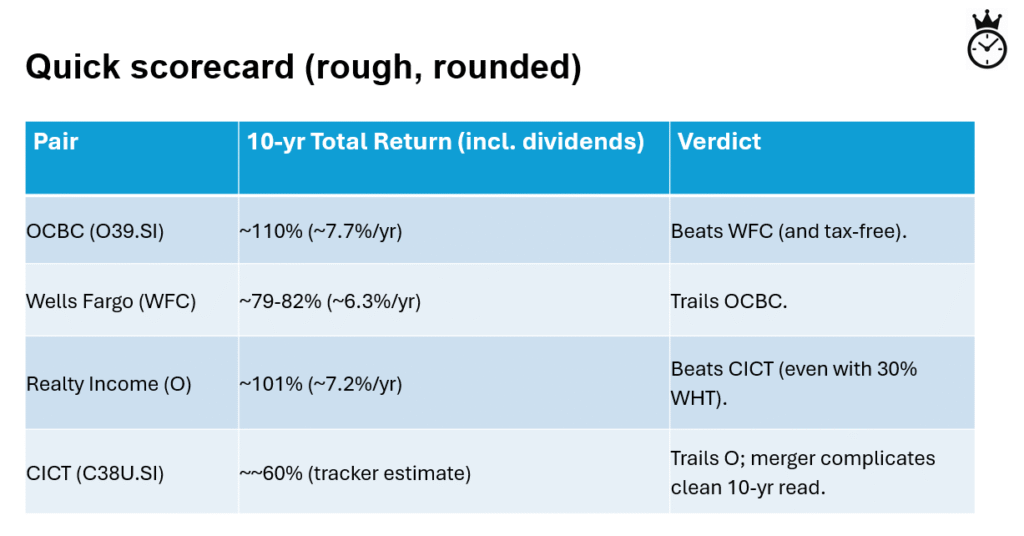

- OCBC: A $20k investment 10 years ago grew to ~$41.8k, a total return of ~110% (~7.7% annualized).

- Wells Fargo: 10-year total return ~79–82%, ~6.3% annualized. (Data varies slightly by source snapshot; both are in this ballpark.)

Takeaway: Despite OCBC’s higher headline dividend tax advantage, what’s striking is simply that OCBC outperformed WFC on total return over the decade, even before we consider US withholding tax. (WFC’s multi-year scandal overhang and dividend reset after 2020 didn’t help.)

2) REIT vs REIT:

CICT (C38U.SI)

vs

Realty Income (O)

- Realty Income (O): 10-year total return ~101%, ~7.2% annualized. Monthly dividends kept compounding even through rate shocks.

- CICT (C38U.SI): Public sources that track total return suggest materially lower 10-year results (one tracker shows ~62% including dividends), with better numbers over 5 years (~42% TSR) as post-merger assets stabilized. Note: CICT’s history includes the 2020 merger (CMT + CCT), which makes “pure” 10-year apples-to-apples a bit messy—but directionally, CICT trails O over the decade.

Takeaway: For REITs, the US name (O) outpaced CICT on decade-long total return, even after acknowledging US dividends suffer 30% withholding for Singapore investors.

So… do US dividend stocks still “win” despite the 30% tax?

It depends on the sector and the specific stock. Here’s the nuance:

- Banks: In this comparison set, OCBC beat WFC on a 10-year total return basis. The tax advantage in Singapore sweetens the net result further.

- REITs: Realty Income beat CICT over 10 years on total return. Even after factoring the 30% dividend haircut, O’s dividend growth history and scale still left it ahead.

Generalising beyond these four tickers:

The US market has a much deeper bench of dividend growers with long records of dividend and earnings growth, which often drives higher total returns over time, despite the withholding tax. But it’s not a blanket rule: as the bank example shows, a strong Singapore blue chip can absolutely outperform a US peer over a given decade.

What drove the differences?

Dividend growth vs. yield

- US dividend growers (e.g., O’s long history of raises) compound faster than high-but-flat payers. Compounding can overwhelm the 30% tax drag over long holding periods.

- CICT’s headline yield is high today, but distribution growth has been modest across the last decade amid rising rates and the 2020 merger transition.

Earnings power and reinvestment runway

- OCBC benefited from solid profitability and dividend progression;

- WFC faced regulatory caps and scandal fallout, dampening total return.

Interest-rate sensitivity

- REITs globally were hit by the 2022–2024 rate surge. Scale and cost of capital matter; O navigated it better than many, while Singapore REITs faced refinancing and valuation pressure.

Practical takeaways for a SG-based dividend investor

- Use total return as the scoreboard. A 6–8% US dividend grower can beat a 7–8% static yielder in Singapore over time, even with 30% WHT if dividend and earnings growth persist.

- Exploit SG tax perks where quality & growth exist. OCBC shows that Singapore blue chips can out-compete US peers on a 10-year view and your dividends come in tax-free.

- Mind structure and history. CICT’s 10-year read is complicated by a 2020 merger; always check whether you’re comparing like-for-like periods and entities.

- Think portfolio, not passport. Mix SG names (to harvest tax-free income) with select US dividend growers (for long-term compounding). Reinvest dividends where possible to let compounding do its work.

Notes: Different data vendors may show slight variations due to date cutoffs and reinvestment assumptions. REIT/Trust histories (like CICT) can be affected by mergers and corporate actions.

Final word

Does the US still “out-win” Singapore after 10 years?

Sometimes, but not always. In this four-stock face-off, US beats SG for REITs, while SG beats US for banks. The lesson: let quality + growth lead, and use tax as a tiebreaker – not the starting point.

Source:

- The Smart Investor

- Dr. Wealth

- IRS

- FinanceCharts

- Gllt.morningstart.com

- Simply Wall St

Like what you see? Share it!

Discover more from BOSS OF MY TIME (BOMT)

Subscribe to get the latest posts sent to your email.