How a regular 9-to-5 employee earns passive income for financial independence

My Watchlist: 5 Dividend Stocks I’m Watching in 2025 (And Why)

If dividend investing has taught me anything, it’s that patience and process matter more than impulse. Instead of buying at the first hype, I keep a lean watchlist of robust companies – ones with reliable dividends, solid fundamentals, and durable advantages.

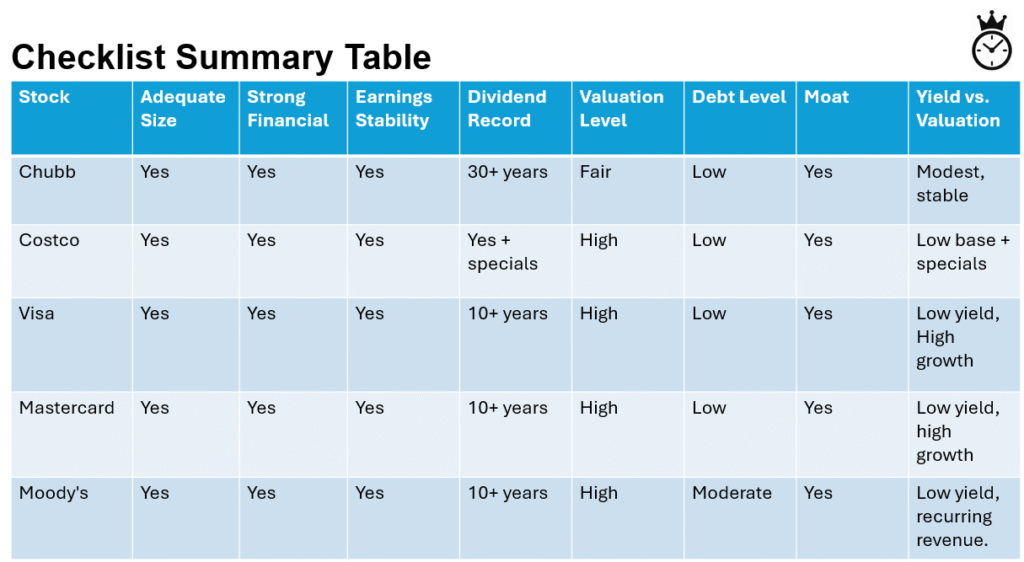

Today, I’m spotlighting five companies that fit the bill: Chubb, Costco, Visa, Mastercard, and Moody’s. I’ve evaluated each using my 30-minute dividend stock checklist to show how they measure up.

This is not a buy list or financial advice, just my personal watchlist based on the fundamentals as they stand today. Businesses change, so I always review and adjust my list if their fundamentals shift.

1. Chubb (CB) — Insurance Built on Discipline

- Adequate Business Size: A global insurance powerhouse with significant scale.

- Strong Financials: Consistently posts low combined ratios and maintains a healthy balance sheet.

- Earnings Stability: Underwriting discipline results in steady, predictable earnings.

- Consistent Dividend: Over 30 consecutive years of dividend growth.

- Reasonable Valuation: Typically trades at mid-teens P/E, a fair range for its sector.

- Low Debt: Conservative debt-to-equity ratio.

- Economic Moat: Strong capital base, underwriting expertise, and global brand.

- Valuation vs. Yield: Yield around 1–2%, modest but backed by stability.

Why I’m Watching: Insurance isn’t flashy, but Chubb’s stability, prudent management, and dividend growth make it a cornerstone-quality holding.

2. Costco (COST) — The Retail Model Reinvented

- Adequate Business Size: A retail and membership giant with global presence.

- Strong Financials: Low debt, steady membership-driven cash flow.

- Earnings Stability: High renewal rates and consistent same-store growth.

- Consistent Dividend: Modest yield, but occasional special dividends reward shareholders.

- Valuation Fit: High P/E due to quality and consistent performance.

- Low Debt: Conservative balance sheet.

- Moat: Membership loyalty, bulk buying power, and supply chain efficiency.

- Valuation vs. Yield: Low base yield but occasional special payouts make it attractive.

Why I’m Watching: Costco’s subscription-style model ensures reliable cash flow and long-term resilience.

3. Visa (V) — Payment Powerhouse in Growth Mode

- Adequate Business Size: One of the largest payment networks worldwide.

- Strong Financials: Asset-light model with high margins and consistent cash generation.

- Earnings Stability: Predictable growth driven by global shift to digital payments.

- Consistent Dividend: 10+ years of consecutive growth.

- Valuation Profile: Above-average P/E, but supported by earnings momentum.

- Low Debt: Solid balance sheet.

- Moat: Network effects and brand trust.

- Valuation vs. Yield: Yield under 1%, but backed by high dividend growth.

Why I’m Watching: A low-yield but high-growth dividend play on the global cashless trend.

4. Mastercard (MA) — Another Leader Riding Cashless Trends

- Adequate Business Size: Global scale and brand recognition.

- Strong Financials: Excellent ROE, high profit margins, strong cash flow.

- Earnings Stability: Steady revenue growth tied to card transactions.

- Consistent Dividend: 10+ years of increases.

- Valuation: Premium multiple similar to Visa.

- Low Debt: Prudent leverage.

- Moat: Strong network effects and partnerships worldwide.

- Valuation vs. Yield: Low yield but high growth trajectory.

Why I’m Watching: A twin to Visa, with similar growth prospects and network advantages.

5. Moody’s (MCO) — The Ratings & Analytics Boss

- Adequate Business Size: Leading global credit ratings and analytics firm.

- Strong Financials: High margins, recurring revenue, strong free cash flow.

- Earnings Stability: Resilient earnings across market cycles.

- Consistent Dividend: Over 10 years of steady increases.

- Valuation: Premium P/E tied to high-margin growth.

- Moderate Debt: Well-managed leverage.

- Moat: Regulatory barriers, brand trust, and specialized data expertise.

- Valuation vs. Yield: Sub-1% yield, but underpinned by robust fundamentals.

Why I’m Watching: A high-quality, recurring-revenue compounder with entrenched market position.

Final Thoughts

These five companies tick most, or all boxes in my 30-minute dividend stock framework. None of them are yield-heavy, but they are quality compounders with durable advantages and consistent dividend growth.

Rather than chasing market fads, I prefer patiently watching these companies and acting only when the fundamentals and valuation align.

Find out more:

Note & Disclaimer: This watchlist reflects my personal view as of the date of writing. Company fundamentals can change, sometimes quickly. I review my watchlist regularly and make adjustments if a business shows signs of deterioration or fundamental improvement. This article is for informational purposes only and is not financial advice. Please do your own due diligence before investing.

Like what you see? Share it!

Discover more from BOSS OF MY TIME (BOMT)

Subscribe to get the latest posts sent to your email.