How a regular 9-to-5 employee earns passive income for financial independence

The Role of Luck in Financial Independence (And How to Tilt the Odds in Your Favor)

When I look back on my journey to financial independence, I can’t deny that luck played a part. Some events worked in my favor, others didn’t. I started investing at a time when opportunities were plenty. I had a stable job, good health, and a supportive family. Not everyone gets those advantages.

But here’s what I’ve learned: while luck may open doors, discipline and consistency are what keep those doors open long enough for you to walk through. You can’t control luck but you can tilt the odds in your favor by putting yourself in a position to benefit when luck shows up.

Luck Is Real - But It’s Not Everything

It’s easy to look at someone who achieved financial independence and assume they got lucky – that they bought the right stock at the right time or had a higher income to begin with. There’s some truth to that. Timing and circumstances can make a difference.

But luck alone doesn’t create lasting success. I’ve seen high earners who struggle to save, and people who received windfalls only to lose it all. On the other hand, I’ve met average-income earners who built solid portfolios through patience and discipline.

The difference often comes down to what they did with their opportunities. Luck might start the engine, but habits keep the car moving.

The Luck You Can’t Control

Let’s be honest – some parts of life are simply out of our control:

- When and where we’re born. Economic cycles, job markets, and cost of living vary by country and era.

- Family background. Some start with debt, others with a safety net.

- Health. A major illness can derail even the best financial plan.

- Market timing. You can’t predict whether your first decade of investing will be a bull run or a downturn.

These things shape our starting points, but they don’t define our outcomes. What matters is what we do with the hand we’re dealt.

The Luck You Can Influence

While we can’t control luck itself, we can influence how ready we are when opportunity appears. Over time, the more prepared you are, the more “luck” seems to come your way.

Here’s how I’ve learned to tilt the odds in my favor:

1. Live Below Your Means

This is where everything begins. When you consistently spend less than you earn, you give yourself room to move – to save, invest, and seize opportunities when they appear.

In my early years, I didn’t have huge pay raises or windfalls. But by keeping expenses modest, I was able to save and invest regularly. That discipline became my version of “manufactured luck.”

You can’t control when the market dips, but you can control whether you have the cash to take advantage of it.

2. Stay Invested and Consistent

You don’t need perfect timing – you just need time.

Markets move in cycles, but compounding works quietly in the background. The longer you stay invested, the greater your chances of catching those “lucky” upswings.

When my dividend portfolio dropped nearly 50% during the COVID-19 crash, I didn’t panic. I continued buying quality companies, even when the headlines screamed fear. Looking back, that decision made all the difference. Some might say I got lucky with the rebound – but the truth is, I just stayed the course.

3. Keep Learning

Knowledge has a way of attracting luck. The more you learn about investing, the more you recognize opportunities others overlook.

My shift toward dividend investing wasn’t random. It came after years of observing what worked for me and what didn’t – chasing high yields, for example, taught me that reliability matters more than excitement.

Every book, podcast, and annual report I read added another piece to the puzzle. The more I learned, the “luckier” I seemed to get.

4. Build a Margin of Safety

Not all luck is good luck. Sometimes bad luck strikes – job loss, illness, or unexpected expenses. That’s why a margin of safety is essential.

For me, that margin comes from three things:

- Keeping an emergency fund,

- Maintaining insurance to protect against large, unexpected costs, and

- Avoiding unnecessary debt.

I often think of it like sailing: you can’t control the wind, but you can patch the holes in your boat so that even when storms hit, you stay afloat.

5. Play the Long Game

Luck feels random in the short term, but predictable over decades.

If you keep saving, keep investing, and keep learning, your odds of success grow with time. The market rewards patience and punishes impulsiveness and the data proves it.

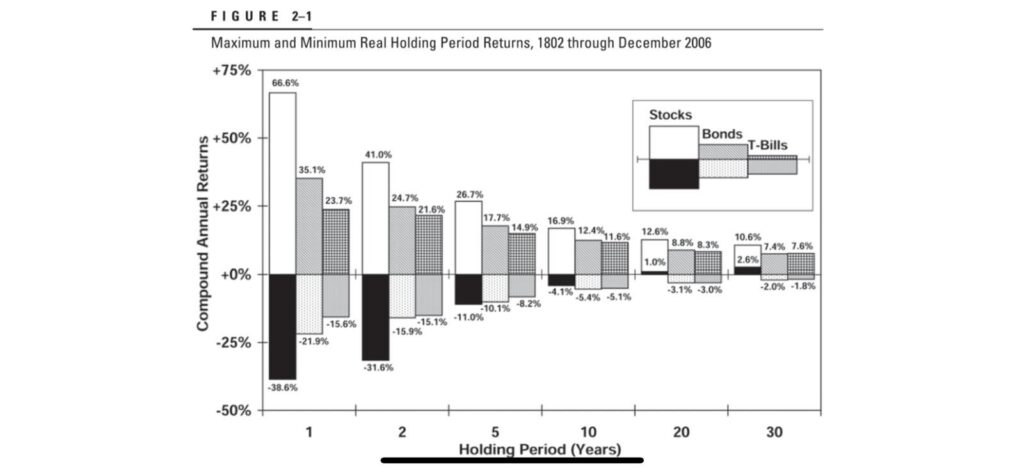

One of my favorite illustrations comes from Jeremy J. Siegel’s classic, Stocks for the Long Run. The chart below shows the maximum and minimum real returns for stocks, bonds, and T-bills over different holding periods – from 1 year all the way to 30 years.

Source: Jeremy J. Siegel, Chapter 2 “Risk, Return, and Portfolio Allocation,” Stocks for the Long Run. McGraw Hill. DOI: 10.1036/0071494707.

The takeaway is powerful:

- Over 1-year periods, stock returns ranged wildly from +66.6% to –38.6%.

- But over 30-year periods, that range narrowed dramatically to +10.6% to +2.6%.

In other words, the longer you stay invested, the less luck matters. The extremes smooth out. Volatility fades. Time becomes your biggest ally.

This is why I never obsess over short-term price swings. Over a single year, luck can make you look smart or foolish. Over 20 or 30 years, discipline and patience make you look wise.

So instead of trying to time the market or chase quick wins, I focus on staying invested through every cycle. Because the real “luck” in investing isn’t catching the next rally – it’s being around long enough for compounding to do its work.

Why “Unlucky” People Often Stay Stuck

I’ve heard people say, “It’s easy for others – they just got lucky.” But often, it’s not bad luck holding them back – it’s short-term decisions that never allow luck to work in their favor.

Selling at the first sign of red.

Upgrading lifestyle as income rises.

Ignoring investing because the market looks uncertain.

These choices block luck from compounding. The opportunity might appear, but without savings, discipline, or courage, they can’t take advantage of it.

Recognizing Luck Without Relying on It

It’s important to acknowledge luck where it exists. I know I’ve had my share – a steady income, supportive spouse, and reasonably good timing in my investing years. Not everyone gets that combination.

But I also know many people who started with more advantages and didn’t achieve financial independence. The difference isn’t luck – it’s what you do with it.

Acknowledging luck keeps me humble and grateful. It reminds me not to get complacent, and to keep preparing for the next phase of the journey.

Final Thoughts: Stack the Odds in Your Favor

Luck will always play a part in financial independence. But it’s not the main character – it’s just one of

the supporting roles.

If you build good habits, protect your downside, and stay consistent, you’ll naturally attract more opportunities over time. The market might surprise you. A new income stream might appear. Or an idea might suddenly click. When that happens, you’ll be ready – not because of chance, but because of preparation.

As the saying goes:

“Luck is what happens when preparation meets opportunity.”

So don’t sit around waiting to get lucky. Start building the habits that make luck matter.

Because the harder you work, the luckier you’ll seem.

Like what you see? Share it!

Discover more from BOSS OF MY TIME (BOMT)

Subscribe to get the latest posts sent to your email.